COFORGE: Growth, no matter what, TP INR1900, 30% Upside, Buy: BY Motilal Oswal Research

MUMBAI, 17 JUNE: We attended Coforge’s Analyst Day, where discussions were centered on the company’s medium-term growth aspirations, margin outlook following the Encora acquisition, evolving commercial models and the role of AI across its key verticals. Management outlined its ambition to scale up revenue from ~USD2.5b currently to ~USD5b by FY30, implying a revenue CAGR of ~19% (~15% organic), supported by deeper penetration within existing verticals, increasing wallet share in large accounts, sustained large-deal momentum, and selective acquisitions. The company also indicated that its margin profile has structurally improved, with portfolio rationalization, acquisition integration and productivity initiatives supporting margins at levels above historical averages.

We came away with the view that Coforge is attempting to evolve beyond a purely volume-led growth model. Management increasingly emphasized domain-led transformation programs, outcome-oriented commercial structures, and larger, proactive engagements across key verticals such as Banking (29% of revenue) and Travel (25% of revenue). While the medium-term ambition appears achievable given the company’s execution track record, sustained delivery will depend on successful large-deal conversion, integration of acquisitions and continued monetization of AI-led opportunities. We continue to view COFORGE as a structurally strong mid-tier player and reiterate it as our top pick. We value COFORGE at 26x FY28E EPS with a TP of INR1,900, implying a 30% potential upside. Reiterate BUY.

Revenue outlook: Growth aspirations supported by vertical depth, deal momentum and acquisitions

‐ Management outlined an ambition to scale up revenue from ~USD2.5b currently to ~USD5b by FY30, implying a revenue CAGR of ~19% (organic revenue growth of 15%; see Exhibit 1). The growth framework is built around deeper penetration within existing verticals, increasing wallet share in large accounts, and selective acquisitions.

‐ The next leg of growth is expected to be driven by scaling up existing franchises rather than building new businesses. Management expects Banking to expand from ~USD625m currently toward ~USD1b, Travel from USD511m toward USD850m, Insurance from USD321m toward USD550m, and Healthcare & Hi-Tech from ~USD402m toward ~USD750m over the planning period.

‐ Large deals remain an important source of visibility. The number of large deals increased to 21 in FY26 from 11 in FY22, while the 12-month executable order book expanded to ~USD1.75b from ~USD720m over the same period. Management also highlighted that order intake has nearly doubled over the last four years.

‐ We believe the key takeaway is that Coforge is attempting to move beyond a purely volume-led growth model. Increasing wallet share within large accounts, embedding AI into transformation programs, and expanding outcome-oriented engagements could gradually improve the quality and durability of growth. That said, execution around large-deal conversion, acquisition integration, and AI monetization will remain key monitorables.

Margins: FY26 could mark a structural reset in the margin profile

‐ Management argued that FY26 margin expansion reflects structural changes in the business rather than temporary one-offs. FY26 EBITDA margin expanded to 18.6% (+430bp YoY), while EBIT margin improved to 14.4% (+370bp YoY), supported by portfolio actions, AI-led productivity improvements, and integration benefits from acquisitions.

‐ Importantly, management referred to the current profitability profile as the ‘new normal’, with FY27E EBITDA margin indicated at ~20.5% (consolidated) and EBIT margin at ~16.5% (standalone, ex-Encora) and ~15.5% on a consolidated basis.

‐ As seen in Exhibit 4, several structural initiatives have contributed to the margin reset. The exit from AdvantageGo added ~60bp to EBIT margins while improving cash conversion; the wind-down of the India government business removed a lower-margin revenue stream; and Cigniti’s EBITDA margin improved from ~12% at acquisition to ~21% within five quarters.

‐ Management also highlighted productivity gains across delivery and support functions, with internal AI deployment helping sustain gross margins and reduce G&A costs. In parallel, AI-led delivery constructs such as Mod Squads are already generating measurable productivity gains across modernization and application-management programs.

‐ Overall, we believe Coforge’s margin profile appears structurally stronger than its historical levels. That said, continued investments in sales capabilities, AI assets, partnerships, and talent could mean that margin progression may not be linear.

Cash flow and capital allocation: Growth investments remain the priority

‐ Following the Encora acquisition, management plans to repay the associated ~USD550m debt over three years, with repayments commencing from 3QFY27. The debt carries a fixed interest rate of ~4.6%.

‐ At the same time, Coforge intends to continue investing in client relationships, alliances and selective acquisitions. Incessant’s revenue expanded from ~USD12m to ~USD120m over the past decade, while Whishworks grew from ~USD27m to ~USD70m with a broader global delivery footprint.

‐ Similarly, SLK reduced client concentration and expanded across geographies and verticals, while Cigniti improved EBITDA margins from ~12% at acquisition to ~21% within two years. These examples suggest that acquisitions remain an important lever not only for expanding capabilities and client access but also for enhancing profitability over time.

‐ The company reiterated that acquisitions remain an important component of its growth strategy, particularly where targets bring in stronger client relationships, domain expertise or access to new markets.

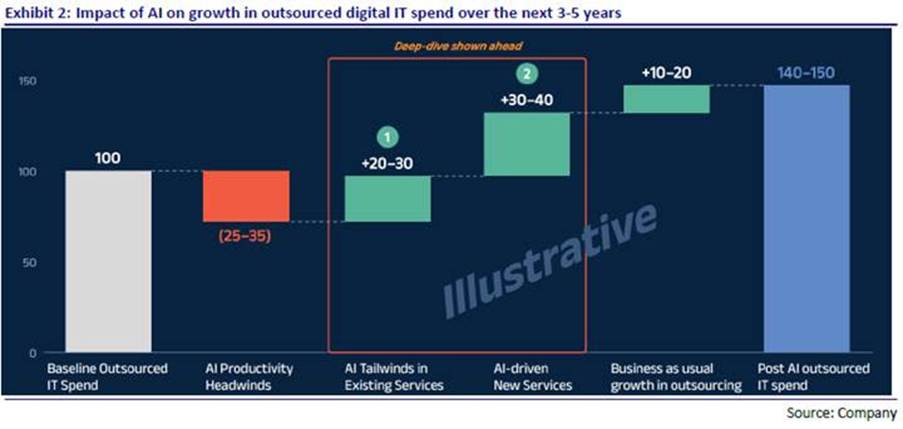

Vertical depth increasingly becoming the foundation for AI-led growth

‐ Coforge’s differentiation increasingly appears to lie at the intersection of deep industry expertise and AI-led delivery. Across Banking, Insurance and Travel, the company showcased industry-specific assets aimed at solving business problems through a combination of domain knowledge, AI and modernization capabilities.

‐ In Banking and Insurance, Coforge introduced several AI-led assets focused on areas such as wealth management, underwriting, claims processing and modernization.

‐ The company has also invested in industry-specific knowledge layers, including Lexicon in Banking and Nexa in Insurance, designed to improve contextual understanding, governance and the effectiveness of agentic workflows. We believe these capabilities could strengthen Coforge’s positioning in increasingly outcome-oriented transformation programs.

‐ Travel remains one of Coforge’s strongest verticals, supported by relationships spanning 60+ airlines and execution experience across 20 passenger service system (PSS) migrations. The company’s travel offerings are increasingly centered around modernization, retail transformation and AI-enabled traveler experiences.

‐ We believe Coforge appears to be positioning itself around the intersection of domain expertise, reusable assets and AI-led transformation rather than generic AI implementation. The ability to scale up these assets into larger engagements and sustained revenue streams will remain the key monitorable.

Commercial models evolving alongside AI adoption

‐ Across multiple sessions, management highlighted that transformation conversations increasingly extend beyond the CIO to include business leaders responsible for growth, customer experience and operating outcomes.

‐ As a result, commercial structures are also evolving. Traditional effort-based contracts are gradually being supplemented by outcome-linked models, including gain-sharing and revenue-linked arrangements.

‐ Management believes that stronger domain expertise improves its ability to participate in these discussions, particularly where technology investments are directly tied to business KPIs.

‐ Large-deal momentum reflects this shift. FY26 large-deal TCV increased ~38% YoY to USD629m, while win rates improved from 38% to 47%, supported by earlier client engagement and stronger solution alignment.

‐ We think the nature of large deals may continue to evolve. Future opportunities could increasingly combine legacy modernization, domain platforms, AI assets and outcome-linked commercials under a single transformation umbrella. Coforge appears to be positioning itself accordingly.

Valuation and view

‐ We expect COFORGE to be the growth leader within our coverage universe and we reiterate it as our top pick.

‐ The analyst day reinforced our confidence in Coforge’s medium-term growth outlook. Management outlined its ambition to scale up revenue to ~USD5b by FY30, supported by increasing wallet share within key accounts, healthy large-deal momentum, deeper penetration across core verticals, and a structurally stronger margins profile.

‐ We continue to view COFORGE as a structurally strong mid-tier player, supported by an improving margin profile, strong deal wins, and consistent growth outperformance. We value COFORGE at 26x FY28E EPS with a TP of INR1,900, implying a 30% potential upside. We reiterate our BUY rating on the stock.

(Disclaimer: The information provided here is investment advice only. Investing in the markets is subject to risks and please consult your advisor before investing.)

(સ્પષ્ટતા: અત્રેથી આપવામાં આવતી તમામ પ્રકારની માહિતી કોઇપણ પ્રકારે રોકાણ/ ટ્રેડીંગ માટેની સલાહ નથી. બજારોમાં રોકાણ જોખમોને આધીન છે અને રોકાણ કરતા પહેલા કૃપા કરીને તમારા સલાહકારની સલાહ લો. વધુમાં અત્રે પ્રગટ થયેલા કોઇપણ સમાચાર કે વિગતો સાથે businessgujarat.in અંશતઃ કે સંપુર્સણપણે સહમત નથી.)