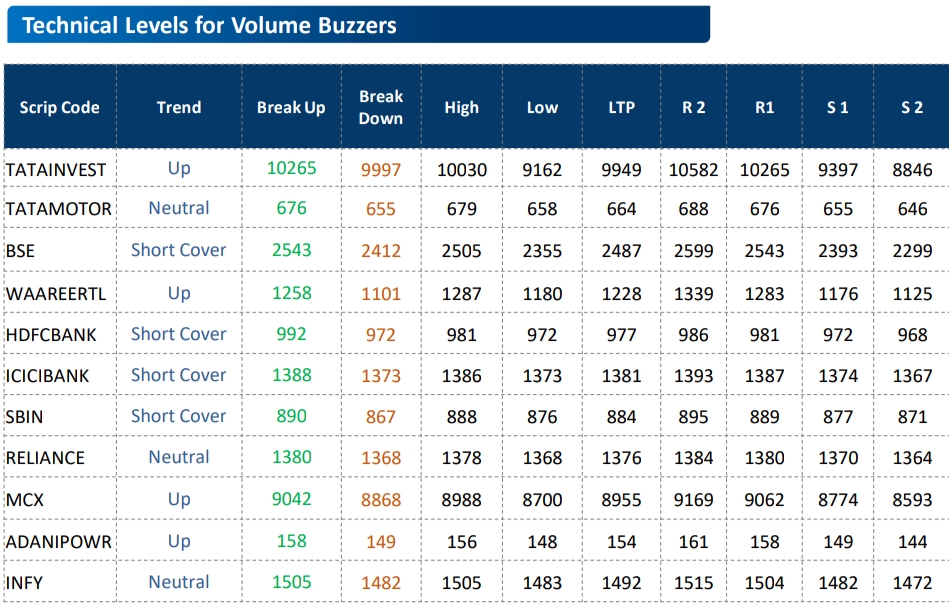

BROKERS CHOICE: LGELECTRONICS, HCLTECH, JUSTDIAL, RIL, SBI, MCX, INFY, ADANIPOWER

MUMBAI, 14 OCTOBER: અગ્રણી બ્રોકરેજ હાઉસ તથા ફંડ હાઉસ તરફથી પસંદગીના સ્ટોક્સમાં ખરીદી\ વેચાણ\ હોલ્ડ કરવા માટે ભલામણ કરવામાં આવી છે. તે રોકાણકારોના અભ્યાસ માટે અત્રે રજૂ કરીએ છીએ.

MOSL on LG Electronics: initiates to Buy on Company, raise target price at Rs 1800/Sh (Positive)

MOSL on HCL Tech: Maintain Buy on Company, target price at Rs 1800/Sh from 1750/sh (Positive)

Jefferies on HCL Tech: Maintain Buy on Company, target price at Rs 1730/Sh (Positive)

GS HCL Tech: Maintain Neutral on Company, target price at Rs 1620/Sh from 1530/sh (Positive)

MS on HCL Tech: Equal Weight on Company, target price at Rs 1680/Sh (Neutral)

Nuvama on HCL Tech: Maintain Hold on Company, target price at Rs 1650/Sh from 1630/sh (Neutral)

Nuvama on Just Dial: Maintain Buy on Company, target price at Rs 1200/Sh from 1280/sh (Neutral)

Citi on HCL Tech: Maintain Neutral on Company, target price at Rs 1600/Sh (Neutral)

MOFSL | MOrning India (14/October/25): LG Electronics India

CMP: INR1,140 TP: INR1,800 (+58%) Buy

Focus on premiumization, localization, and higher export/B2B revenue

High industry growth potential; holds leadership position: India’s home appliances

and consumer electronics market (excluding mobile phones) is estimated to post a

CAGR of ~14% over CY24-29. LG Electronics India (LGEIL), with its leadership across

key product categories, is well-positioned to capitalize on this growth

opportunity. The company plans to balance between premium and mass products

as part of LG’s global strategy and aims for premiumization of mass products,

which should help to improve affordability and, in turn, increase its customer

base.

Focus on export; higher B2B and AMC segment revenue: The company plans to

raise its export share to ~10% by FY28E from 6% in FY25. It also aims to generate

14-15% of its revenue from the B2B segment over the next few years (vs. ~10% in

FY25), noting that B2B margins are higher than those in the B2C segment. Further,

LGEIL targets an over 25% YoY growth in AMC revenue for the next few years.

Premiumization and localization drive profitability: LGEIL’s strategic focus on

premiumization has resulted in innovative launches across OLED TVs, inverter ACs,

and advanced smart appliances. The company holds strong market positions in

premium segments, such as OLED TVs (~63%), front-load washing machines

(~37%), and side-by-side refrigerators (~43%). The share of raw materials sourced

domestically stood at ~54% in FY25, with plans to increase this to ~63% over the

next four years. This will also lead to an improvement in gross margin.

Extensive distribution network; focus on brand building and localization:

Distribution remains a key competitive strength for LGEIL, with 35,640 B2C

touchpoints, 777 exclusive brand shops, and 463 B2B trade partners in 1QFY26.

The company also operates one of India’s largest after-sales networks, comprising

1,006 service centers. It allocates ~4.5% of its revenue to advertising and

promotion (A&P) expenses, which we expect to continue until FY28.

Strong fundamentals; initiate coverage with a BUY rating: We expect LGEIL to

trade at higher multiples, given: 1) strong return ratios (RoE/RoIC of ~30%/66% in

FY28E); 2) higher OCF conversion, averaging ~74% during FY26-28E; 3) a strategic

focus on localization, which is expected to further expand gross margin; 4)

targeted growth in high-margin B2B and AMC business; and 5) a leadership

position across key product categories. We initiate coverage on LGEIL with a BUY

rating and a TP of INR1,800, premised on 40x FY28E EPS.

Key downside risks: 1) any increase in royalty by the parent company, LG

Electronics Korea, 2) volatile raw material prices, and 3) intensifying competition.

Strong industry tailwinds, leadership position, and export potential

India’s home appliances and consumer electronics market is projected to

post a CAGR of ~11% over CY24-29, reaching ~INR11t by CY29. Excluding

mobile phones (LGEIL exited this segment in FY23), the market is estimated

to clock a 14% CAGR during CY24-29. As a market leader in major categories,

LGEIL is well-placed to benefit from this strong industry growth momentum.

LGEIL holds strong offline market shares in key consumer durables

categories, such as TVs, washing machines, refrigerators, ACs, ovens, and

water purifiers. The company holds a market share (in terms of value in the

offline channel during 1HCY25) of ~28% in panel televisions, ~34% in

washing machines, ~30% in refrigerators, ~21% in inverter AC (~18% in RAC),

~51% in microwave ovens, and ~41% in water purifiers.

(Disclaimer: The information provided here is investment advice only. Investing in the markets is subject to risks and please consult your advisor before investing.)

(સ્પષ્ટતા: અત્રેથી આપવામાં આવતી તમામ પ્રકારની માહિતી કોઇપણ પ્રકારે રોકાણ/ ટ્રેડીંગ માટેની સલાહ નથી. બજારોમાં રોકાણ જોખમોને આધીન છે અને રોકાણ કરતા પહેલા કૃપા કરીને તમારા સલાહકારની સલાહ લો.)