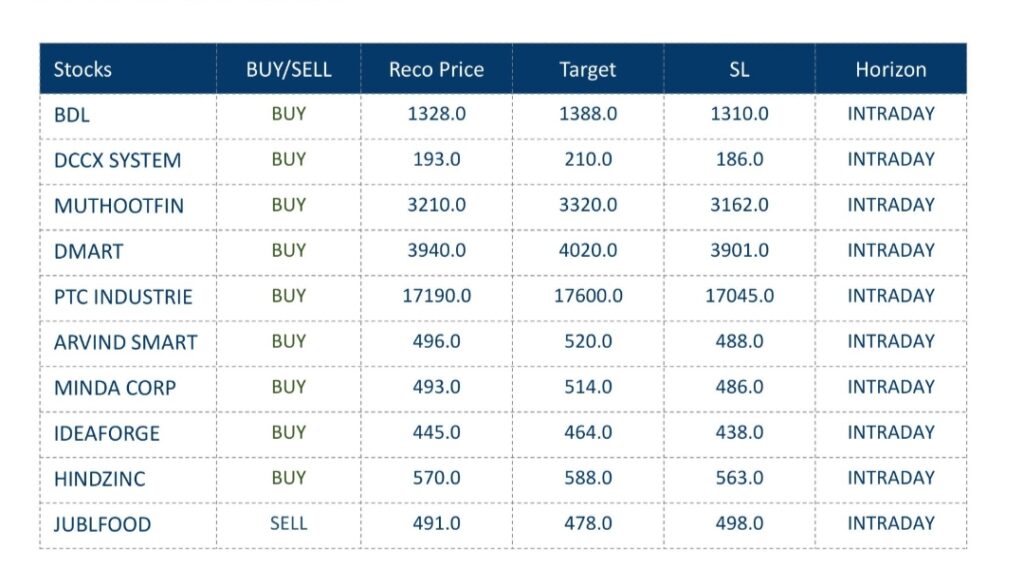

BROKERS CHOICE: KIMS, LG, RELIANCE, IOC, MEESHO, BPCL, SBIN, ADANI, HDFCBANK, ONGC, M&M

AHMEDABAD, 10 MARCH: અગ્રણી બ્રોકરેજ હાઉસ તથા ફંડ હાઉસ તરફથી પસંદગીના સ્ટોક્સમાં ખરીદી\ વેચાણ\ હોલ્ડ કરવા માટે ભલામણ કરવામાં આવી છે. તે રોકાણકારોના અભ્યાસ માટે અત્રે રજૂ કરીએ છીએ.

Jefferies on Amber Ent: Maintain Buy on Company, raise target price at Rs 9120/Sh (Positive)

Jefferies on Uno Minda: Initiate Buy on Company, target price at Rs 1350/Sh (Positive)

Kotak on Escorts: Upgrade to Add on Company, raise target price at Rs 3375/Sh (Positive)

GS on KIMS: Maintain Buy on Company, target price at Rs 875/Sh (Positive)

MS on Apollo Hospitals: Maintain Overweight on Company, target price at Rs 9209/Sh (Positive)

MS on LG India: Maintain Overweight on Company, target price at Rs 1726/Sh (Positive)

Macquarie on Adani Ports: Maintain Outperform on Company, target price at Rs 1760/Sh (Positive)

MS on Reliance: Maintain Overweight on Company, target price at Rs 1803/Sh (Positive)

Incred on Jubilant Ing: Upgrade to Add on Company, target price at Rs 780/Sh (Positive)

Jefferies on Divis Lab: Maintain Buy on Company, target price at Rs 8200/Sh (Positive)

Macquarie on Energy Sector: Coal India benefits from upside risk to e-auction coal price and improved coal demand from power. (Positive)

MS on Energy Sector: Continue to view Indian refiners and OMCs positively and would look to add during underperformance. (Positive)

MOSL on Defence Sector: West Asia conflict likely to drive higher global defence spending, India’s defence sector well positioned on strong domestic procurement & export opportunities. Government push for indigenisation strengthens sector outlook. (Positive)

Jefferies on Tiles Industry: Middle East conflict has constrained domestic Gas supply, as India receives ~75% of LNG via Strait of Hormuz. LNG and Propane account for 70% of fuel to Morbi Tiles industry, which is notably curtailed now (Neutral)

HSBC on Insurance Sector: Ind APE growth rebounds to around 20% YoY in Feb 2026, March volumes may be impacted by volatile markets. Most life insurers report strong pick-up in individual APE on higher policies sold (Neutral)

HSBC on Industrial Sector: Central govt capex declined 25% YoY in Jan 2026 while YTD capex is still up 11% YoY vs revised estimate (RE) of 4% YoY growth. Buy Power T&D and defence in correction (Neutral)

UBS On OMCs: Geopolitical risks cloud earnings visibility, UBS sees parallels with 2022. Higher oil prices pose upside risk, OMCs’ marketing exposure weighs on earnings. (Neutral)

Jefferies on Dixon Tech: Maintain Hold on Company, target price at Rs 11350/Sh (Neutral)

HSBC on Meesho: Maintain Hold on Company, target price at Rs 160/Sh (Neutral)

UBS on IOC: Downgrade to Neutral on Company, cut target price at Rs 175/Sh (Neutral)

UBS on BPCL: Downgrade to Neutral on Company, cut target price at Rs 365/Sh (Neutral)

UBS on Hind Petro: Downgrade to Sell on Company, cut target price at Rs 340/Sh (Neutral)

(Disclaimer: The information provided here is investment advice only. Investing in the markets is subject to risks and please consult your advisor before investing.)

(સ્પષ્ટતા: અત્રેથી આપવામાં આવતી તમામ પ્રકારની માહિતી કોઇપણ પ્રકારે રોકાણ/ ટ્રેડીંગ માટેની સલાહ નથી. બજારોમાં રોકાણ જોખમોને આધીન છે અને રોકાણ કરતા પહેલા કૃપા કરીને તમારા સલાહકારની સલાહ લો.)